The Kids' Camera Paradox: Why a Growing Category Faces Shrinking Margins

The Market Headwinds

1. Smartphone Cannibalization at Ever-Younger Ages

The core demographic for children's cameras — ages 5 to 8 — is being eroded from above. In urban China, over 40% of primary school students now have access to a smartphone or tablet with a camera. In the US and EU, that figure is closer to 50% by age 7. Parents increasingly reason: *why buy a separate camera when the phone already takes better pictures?*

The argument is disingenuous — a dedicated camera is arguably healthier than smartphone access — but it wins in household budget conversations. Every kid with a phone in their pocket is a kid who won't own a dedicated camera.

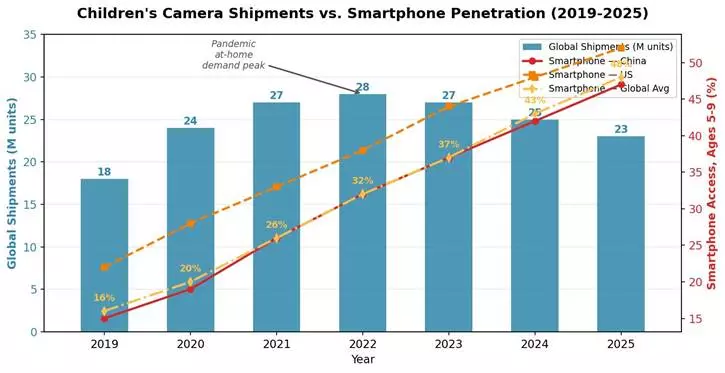

Figure 1: Global children's camera unit shipments (2019-2025) plotted against estimated smartphone access rates among 5-9-year-olds in key markets. Category volume peaked in 2022-2023 at roughly 28 million units shipped, driven by pandemic-era at-home activity demand. Post-2023, shipment volumes are declining as smartphone substitution accelerates — though the premium segment (WiFi-enabled, >8 MP) continues to grow modestly.

2. The ¥29 White-Label Floor

Open Temu, Shopee, or Pinduoduo and search "kids camera." The first page of results will show dozens of listings at ¥29-49 ($4-7 USD). These products use decade-old 0.3 MP sensors, fixed-focus plastic lenses, and unlicensed cartoon character shells. They are functionally disposable — and yet they define the consumer's price anchor.

For a manufacturer producing a properly engineered children's camera — with a drop-rated enclosure, a 5 MP sensor, a replaceable battery, and actual quality control — the factory-gate cost is already ¥40-60 before branding and distribution. Competing on price against the ¥29 units is a race to the bottom nobody wins. The only viable strategy is differentiation: better durability, better image quality, or a feature white-label cameras can't copy (WiFi direct, parental app integration, educational content).

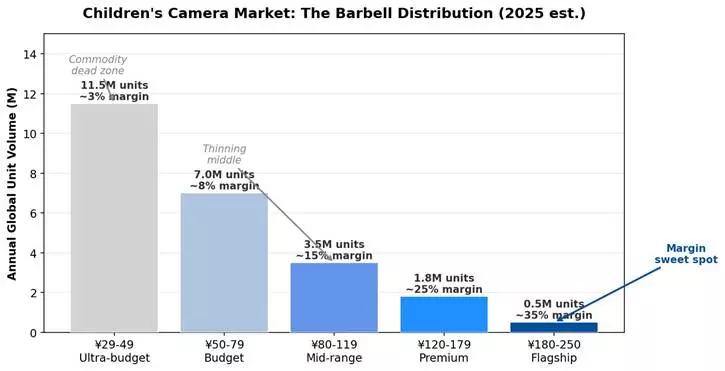

The result is a barbell-shaped market: high-volume commodity trash at the bottom, a small premium segment at the top, and a rapidly thinning middle where most manufacturers compete.

Figure 2: The children's camera market in 2025 exhibits a pronounced barbell distribution. Over 70% of unit volume sits below ¥79 retail — but margins in this segment hover near zero. The premium tier (¥120+) captures only ~8% of volume but offers 25-35% margins. The middle segment (¥80-119), where most branded manufacturers position, is structurally squeezed: too expensive to compete on volume with white-label, too cheap to command premium margins.

3. Shrinking Demographics

China's 2025 birth cohort was approximately 9 million — down from 17.2 million in 2017. Japan, South Korea, and much of Europe face similar or worse demographic trajectories. The children's camera category is structurally tied to the size of the 5-9 age cohort, and that cohort is shrinking by 3-5% annually in most developed and middle-income markets.

For manufacturers, this doesn't mean extinction — but it does mean the business model must shift from volume growth to value capture. The winners will be companies that extract more revenue per unit (via premium features, brand position, or after-sale ecosystem), not companies that try to ship more units.

The Technical Bottlenecks

4. The Durability-Cost Trap

A children's camera must survive: drops from 1.2 meters onto concrete, repeated button mashing, saliva, juice spills, sandbox grit, and being sat on. Meeting even basic drop-test and ingress-protection standards requires TPE overmolding, reinforced ABS shells, silicone button seals, and internal shock-absorbing structures — none of which are free.

The physics of the problem is unforgiving: a camera that can survive a three-year-old costs roughly 30-50% more to manufacture than an equivalent camera without durability engineering. But retailers and consumers punish anything above the ¥120-150 retail price point. The result is a category where every dollar of durability eats directly into margin — and most manufacturers cut corners.

Figure 4: A durability-engineered children's camera featuring TPE overmolding and reinforced ABS shell — the two key cost drivers that separate disposable cameras from ones that survive real-world use. Parents consistently rank durability as their #1 purchase criteria after price.

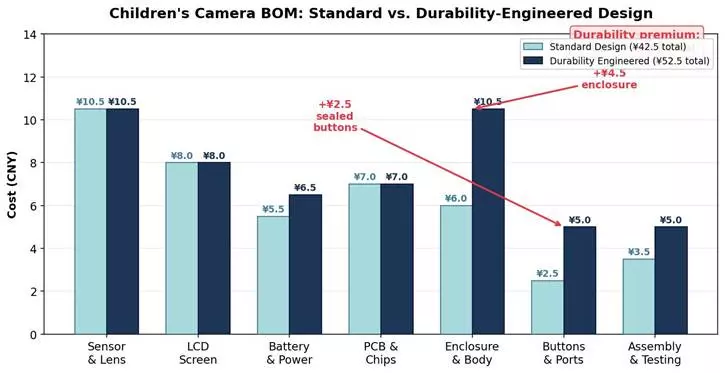

Figure 3: Estimated BOM cost comparison between a basic children's camera (no drop rating, plastic shell, fixed battery compartment) and a durability-engineered model (1.2m drop-rated, TPE overmolding, sealed buttons, replaceable battery with locking door). The durability premium adds approximately ¥12-18 ($1.70-2.50) to factory cost — a 35% increase in a category where total BOM is typically under ¥50.

5. The Image Quality Ceiling

The optical constraints of a children's camera are baked in at the design stage. Small form factor dictates a small lens. Fixed focus is mandatory (kids can't be expected to half-press for autofocus). Aperture is typically f/2.8 — adequate in daylight, useless indoors. The sensor is 5 MP at best, often 2 MP, always 1/3-inch or smaller.

Compare this to a five-year-old smartphone: computational photography pipelines do multi-frame HDR synthesis, AI scene detection, and night mode — automatically, with zero user intervention. The child snaps a photo on a 2022 entry-level smartphone and gets a surprisingly good image. They take the same photo on a dedicated kids' camera and get a grainy, poorly exposed result. That gap in output quality is the single biggest driver of product abandonment — the camera ends up in a drawer after three weeks.

Closing this gap is technically possible (better sensors exist, larger lenses exist), but the BOM math doesn't close at current retail prices. This is the fundamental tension of the category.

6. The Connectivity Conundrum

The user experience parents actually want goes like this: child takes photos → photos appear automatically on parent's phone → parent shares to family group. The user experience most kids' cameras actually deliver is: child takes photos → photos sit on an SD card → parent eventually remembers to pull the card, find a card reader, and manually transfer files → parent never does this.

Adding WiFi to close this gap requires a connectivity module ($2-4 BOM), companion app development (six-figure software investment), and cloud storage infrastructure if the manufacturer wants to offer a complete solution. It also substantially increases power consumption — a WiFi-enabled kids' camera that used to run 4 hours on a charge might run 2 hours with the radio active. Bluetooth Low Energy (BLE) offers a partial fix for photo transfer without the power penalty, but BLE throughput is too slow for bulk image transfer and the user experience remains clunky.

WiFi direct models like Grand Vision's H9S represent the current best compromise — camera acts as a hotspot, parent connects temporarily to download photos, no cloud dependency — but even this approach adds engineering complexity and BOM cost that the category's price point struggles to support.

Figure 5: The connectivity promise — camera captures photos that appear seamlessly on a parent's smartphone. WiFi direct models achieve this without cloud dependency, but the power consumption trade-off and companion app development costs remain significant hurdles for manufacturers operating at the category's tight margins.

What This Means for Buyers and Sourcing

Understanding these six constraints is the difference between picking a product that sells and picking one that collects dust.

Don't compete on price at the bottom. The ¥29-49 segment is a commodity dead zone. If your differentiator is "cheaper," you're competing with factories that have already stripped every possible cost out of the product — including safety compliance and basic quality control.

Durability is the one feature parents will pay for. In consumer perception surveys, "my kid broke it" is the #1 complaint across all children's electronics categories. A camera that survives drops is worth a 30-50% price premium to parents who've already thrown away two cheaper ones. If you can only invest in one area of differentiation, invest in the enclosure.

WiFi/BLE connectivity is a purchase-driver, not a margin-driver. Connected features close sales at the point of comparison shopping, but they don't create pricing power because connectivity is rapidly becoming table stakes in the premium segment. Treat WiFi as a retention feature — it keeps the camera off the shelf — not a margin lever.

Target the demographic trough, not the peak. Markets where birth rates remain healthy (Southeast Asia, Middle East, Africa, parts of Latin America) will be the growth engines of the next decade. Manufacturers that build distribution into these markets now will ride a demographic wave that China and Europe lost years ago.

The Outlook

The children's camera category isn't dying — it's bifurcating. The bottom will continue to be a race-to-zero commodity game dominated by white-label factories with no brand loyalty and no margin. The top will consolidate around a small number of manufacturers who solve the core equation: drop-proof hardware + good-enough optics + seamless connectivity, all at a price parents will pay without hesitation.

That equation is engineering-hard and margin-tight. But for the companies that solve it, the reward is a defensible position in a category where brand trust matters more than raw specifications — and where the customer replaces their purchase every two years as the child grows.

Shenzhen Grand Vision Technology Co., Ltd designs and manufactures children's cameras, action cameras, trail cameras, and night vision devices for global export. Our children's camera line spans entry-level 2 MP models to WiFi-enabled 8 MP drop-rated cameras with parental app integration. For volume pricing, OEM discussion, or specification inquiries, contact sales@grandvisionsz.com.